Strong month for U.S. cheese, WPC80+ exports unable to offset NFDM/SMP and low-protein whey declines.

Regardless of report shipments of WPC80+ and a rebound in U.S. cheese exports, year-over-year U.S. dairy exports (milk solids equal or MSE) fell 12% in September. It was the eighth consecutive decline, relationship again to February 2023.

September export worth fell 25% to $603 million, the bottom month-to-month complete since January 2022.

Traits which were protecting general U.S. exports in verify for many of the 12 months stay largely unchanged. U.S. suppliers proceed to face robust demand headwinds from tepid world financial development, elevated inflation and, within the case of low-protein whey, China’s struggling pork sector (although that reportedly has improved of late). Whereas world milk provide development has slowed, competitors from New Zealand and the EU stays more durable than it has been in recent times.

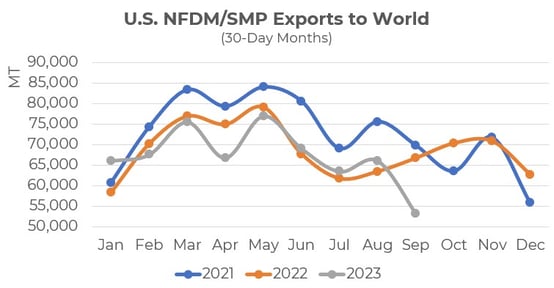

U.S. nonfat dry milk/skim milk powder (NFDM/SMP) exports had their worst month of 2023, falling 20% to 53,256 MT (-13,411 MT). Yr-over-year U.S. shipments to Mexico declined for the primary time in additional than a 12 months (-16%, -5,273 MT). And the nascent restoration in U.S. NFDM/SMP exports to Southeast Asia (+3% for the three-month interval of June-August) ended abruptly in September, with year-over-year quantity falling 38% (-7,314 MT).

China continued to pull down U.S. low-protein whey gross sales. U.S. whey shipments to China (0404.10) fell 39% (-11,427 MT), with across-the-board double-digit declines in dry, whey protein focus (lower than 80%) and modified whey and permeate. U.S. suppliers additionally noticed smaller declines to Mexico (-24%, -928 MT) and Canada (-28%, -1,172 MT).

Gratefully, a number of constructive storylines have emerged in current months and continued into September, notably on the higher-value merchandise.

International cheese demand has confirmed surprisingly resilient internationally, buoyed by the continuing post-pandemic restoration within the foodservice sector and Mexico’s sturdy consumption. Yr-over-year U.S. cheese exports rose 4% (+1,531 MT) in September. Shipments to Mexico remained on report tempo, leaping 26% (+2,524 MT) and U.S. cheese gross sales to China greater than quadrupled (+1,502 MT). U.S. suppliers additionally posted robust beneficial properties to Southeast Asia (+54%, +543 MT), Central America (+10%, +310 MT) and the Caribbean (+9%, +154 MT).

On high of the constructive cheese story, the more and more world dietary attraction of high-protein meals and drinks, coupled with favorable pricing of high-protein whey, drove WPC80+ demand to an all-time excessive. The U.S. shipped 7,356 MT of WPC80+ in September, a 40% enhance (+2,118 MT) over the earlier 12 months. It was the primary time U.S. shipments cleared the 7,000-MT mark—and in a 30-day month no much less. U.S. WPC80+ exports to Japan—our high market—greater than doubled (+1,078 MT) whereas quantity to China greater than tripled (+1,070 MT).

Via three-quarters, on an MSE foundation, U.S. dairy exports have been down 7.5% in comparison with the earlier 12 months. Worth by means of three quarters was $6.23 billion, down 15%.

For a deeper dive into the important thing product classes of cheese and NFDM/SMP, see under.

.png?width=554&height=302&name=Chart101%20(2176%20x%201500%20px).png)

Q3 rebound in cheese exports

After a tough second quarter, U.S. cheese exports returned to impartial in Q3 – reducing simply 16 metric tons in comparison with the 17% (-20,986 MT) decline in Q2. Mexico remained the biggest constructive contributor to U.S. cheese exports in Q3, growing 15% for the quarter and 26% within the month of September because of sturdy client demand and a robust peso. Shredded cheese, particularly, has been the cheese of selection for Mexican patrons, greater than doubling in 2023.

Nonetheless, the foremost change in Q3 was the development in a number of markets apart from Mexico. U.S. cheese exports to Japan went from -29% (-4,358 MT) in Q2 to +15% in Q3 (+1,570 MT); Australia went from +3% (181 MT) to +16% (+878 MT); and gross sales to Central America jumped 23% (+2,060 MT) in comparison with a 17% drop in Q2 (-2,350 MT).

Naturally, not each market was constructive. Gross sales to Korea proceed to be hammered by weak demand and stiff competitors from European suppliers, falling by greater than a 3rd in Q3 (-35%, -6,845 MT). Gross sales to the Center East/North Africa (MENA) dropped by 41% in Q3 (-3,066 MT) for related causes. This distinction between Korea and MENA and most different U.S. markets resulted in cheese commerce holding roughly impartial, which remains to be a marked enchancment from Q2 and is being in contrast in opposition to a report 2022.

So, what drove the development in Q3 after the difficult second quarter?

Actually, value was a serious determinant. As we stated in loads of previous stories, U.S. cheese costs have been uncompetitive for late 2022 and the primary half of 2023 as European cheese costs dropped precipitously and home gross sales and exports to Mexico helped maintain U.S. costs elevated relative to the world market. This naturally led to a pointy drop in Q2, however as U.S. costs declined over the summer season and European costs firmed, exports to extremely aggressive markets like Japan improved.

Happily, U.S. cheese costs have improved for the reason that lows of June and July with roughly comparable costs throughout the foremost exporters, which ought to assist keep the stabilization of U.S. cheese exports into the fourth quarter and 2024, offered world demand improves with a (barely) extra optimistic financial outlook.

NFDM/SMP turns downward once more in September

U.S. NFDM/SMP exports had virtually drawn again to even by means of the primary eight months of 2023, with beneficial properties in June, July and August. Quantity was 558,407 MT—solely 283 MT lower than the earlier 12 months. Nevertheless, a 20% year-over-year shortfall in September dug the year-to-date gap a bit of deeper. U.S. NFDM/SMP exports by means of the primary three quarters have been 611,663 MT, a 2% decline from the primary three quarters of 2022.

September’s weak efficiency stems largely from our two largest patrons—Mexico and Southeast Asia—though the explanations behind every market’s decline diversified.

U.S. shipments to Southeast Asia fell 38% (-7,314 MT) in September to 11,738 MT. The disappointing consequence got here after U.S. suppliers seemed to be rebounding from a longer-term hunch in development to Southeast Asia. U.S. NFDM/SMP exports to the area rose 3% (+2,034 MT) over the June-August interval. Whereas that three-month interval in comparison with a down 12 months in 2022, quantity nonetheless averaged greater than 20,000 MT monthly.

The September outcomes marked a big step down. At 11,738 MT, it was the bottom U.S. month-to-month quantity (30-day months) to the area in six years. Whereas it’s true that New Zealand has been channeling extra milk to butter/SMP, boosting its export provide, the broader problem general is gradual Southeast Asian demand. New Zealand SMP exports to Southeast Asia fell 34% in September and have been down 24% within the third quarter. EU SMP exports to Southeast Asia fell 15% in August (newest accessible information).

Mexico is a unique story. U.S. NFDM/SMP exports to our No. 1 market fell 16% (-5,272 MT) in September. It was the primary year-over-year decline since August 2022. However it didn’t come out of nowhere. U.S. NFDM/SMP exports to Mexico jumped 31% within the first eight months of the 12 months to 286,141 MT—properly on their solution to a brand new annual report. Whereas they’re nonetheless on report tempo, the dimensions of the year-over-year beneficial properties has been dwindling since Could, dropping into the destructive in September.

We see just a few causes behind the slowdown in development, together with the build-up in provide, the worth of the peso and slowdowns on the U.S.-Mexico border that started worsening in September.

The Mexican peso reached a multi-year excessive in opposition to the U.S. greenback in July, making U.S. powder extra reasonably priced. However the peso slowly misplaced worth from July by means of mid-October, overlapping an increase in U.S. NFDM/SMP costs that started in early August.

Enhancements within the peso-U.S. greenback change charge since mid-October present some causes for optimism on NFDM/SMP shipments to Mexico shifting ahead, notably as stalled product is accounted for. However uncertainties stay relating to Southeast Asian demand.

Learn extra about world dairy markets:

The U.S. Dairy Export Council fosters collaborative business partnerships with processors, buying and selling corporations and others to boost world demand for U.S. dairy merchandise and elements. USDEC is primarily supported by Dairy Administration Inc. by means of the dairy farmer checkoff. republish this put up.